USDA Approved Homes for Sale in Maryland

Do you wish you could buy a townhouse, condo or single-family home in Maryland but don’t have the money for a downpayment? If you can’t pay cash for your new home you’ll need a mortgage. Many home buyers think they need a large downpayment to buy a house in Maryland. It’s simply not true. If you don’t have money saved up for a downpayment, the USDA loan might just make it possible to buy a house in certain parts of Maryland. There are specific requirements for a USDA loan. Let’s talk about them, so you can decide if the USDA Maryland loan is right for you.

What is a USDA Loan when Buying a House in Maryland?

What is the USDA loan? The USDA 100% financing (United States Department of Agriculture) loan is a government-backed loan to buy a house with no downpayment. Its purpose is make buying a house more affordable for buyers who don’t a lot of money saved up for a downpayment. It’s perfect for anyone with a low-to-moderate income, a steady job, and good credit. And….it makes it possible to buy a house with very little money out of your pocket! However, the USDA has its own guidelines and requirements, including eligibility requirements for both the homeowner and the property. Lenders will often have their own internal guidelines and requirements in addition to those set by the USDA.

100% financing meaning is sometimes misunderstood, because it sounds too good to be true! It simply means that qualified buyers really can buy a house with no downpayment. They are able to borrow 100% of the purchase price. Buyers will however, need some of their own money to use as their earnest money deposit. And if buyers want to have any inspections done, they will need to pay for those inspections themselves. A termite inspection is one inspection that will be required as part of the loan process.

USDA income and property eligibility are two very important factors in a buyer’s ability to obtain this type of loan. A buyers income must be within a certain range, and a house must be located in a USDA area. We’ll discuss these things in more detail below.

Types of USDA Loans

USDA Guaranteed Loans

Private lenders provide the funds for this loan, and the USDA backs the loan against default. Some specific requirements include:

USDA Direct Loans

The USDA direct loan is designed for low-to-moderate income families so they can have the opportunity to buy a home. The USDA acts as the lender and provides the funds for this loan.

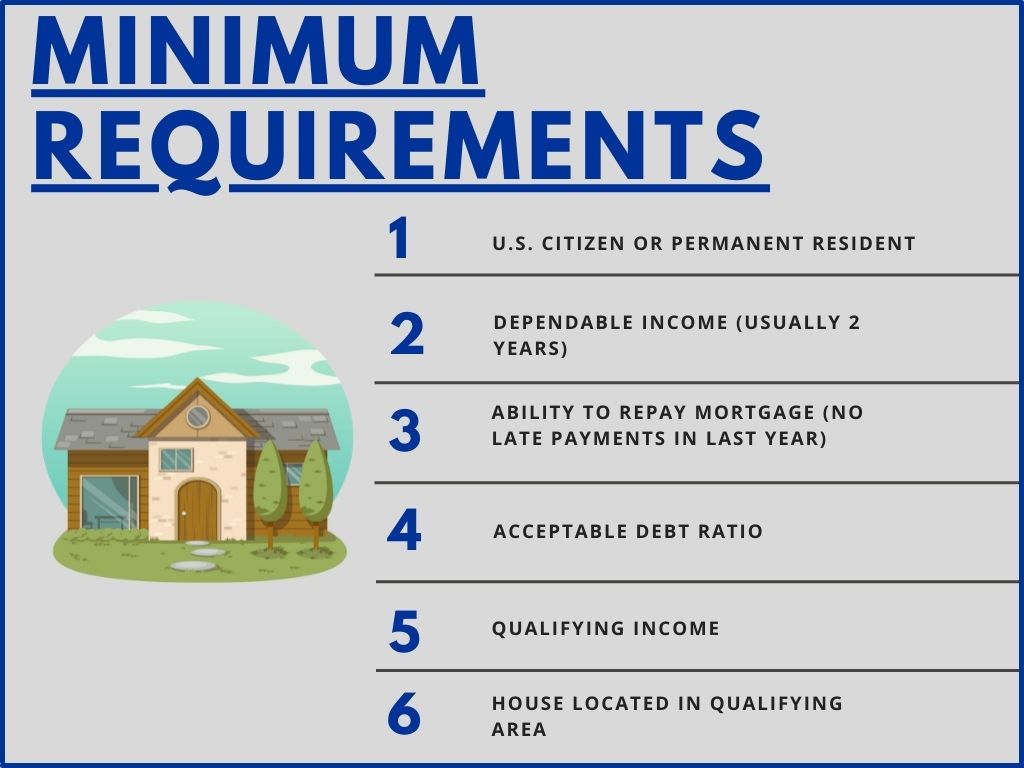

USDA Eligibility / USDA Requirements

For a borrower to be eligible for this type of loan, there are requirements that must be met. Minimum requirements include:

USDA Maryland Income Limits

There is a minimum income limit and a maximum income limit for this type of loan. These limits vary depending on the area where you’d like to buy a house, and the number of people in a household. A larger household (5-8 member household) will have a higher limit than a smaller household (1-4 member household). For example, the limits in Carroll County MD are different from the limits in Montgomery County MD. A trusted lender who works with USDA loans can best advise you on the current limits for each different area in the state of Maryland.

USDA Eligible Areas in Maryland

USDA Loan Map Maryland

To use a USDA loan, the borrower must be purchasing a home in a rural area. The USDA defines “rural” as any town with a population of “25,000 or less that is not adjacent to a large city or that is not part of a continuous urban area.” The home must be “modest” in size. The average USDA home is 1,200 square feet. Homes with swimming pools are ineligible. The loan cannot be used to purchase income producing property, furniture or other personal property, an existing manufactured home or for a home with non-essential buildings and land. To determine if a particular property is eligible, visit the USDA loan map Maryland.

USDA Property Eligibility

In addition to a house being located in a USDA eligible area, the house itself must also meet certain criteria. A buyer’s health and safety is very important to the USDA. This means there can not be any health and/or safety issues in a house. For example, if there are stairs that contain more than 3 steps, there must be a handrail. There can not be any broken windows. There must be, at a minimum, a stove in the kitchen. Speaking of kitchens, there can not be a second kitchen in the house. So….if a house has a second kitchen, and that kitchen contains a stove, it does not qualify for the USDA loan. If a house was built before 1978, there can’t be any peeling paint (neither inside or outside). There can’t be a swimming pool. There can’t be any mold in the house.

How do you know if a house meets the criteria for the USDA loan? A buyer’s agent who has experience with the USDA loan will be able to point out anything in a house that might be a problem for this loan.

USDA Loan Guarantee Fee

What is the USDA loan guarantee fee? When using this type of loan to buy a house, there is a “fee” that must be paid. A portion of the fee (called the upfront fee) is paid as part of the overall closing costs, and is paid at settlement. The secondary part of the fee is an annual fee that is added to the mortgage payment. Fortunately, it can be added to the total loan amount. Yes, this increases the monthly mortgage payment, but prevents a buyer from needing the cash upfront.

The USDA loan guarantee fee refers to how the USDA mortgage is paid and is the equivalent of mortgage insurance. The upfront guarantee fee as of February 2022 is equal to 1% of the loan amount. The annual fee is .35% of the loan amount.

USDA vs Conventional Loan

Is USDA a conventional loan? The answer is no, it is a completely different type of loan. There are three main differences between these 2 types of loans: The conventional loan typically requires a downpayment of at least 3%, and the conventional loan does not have the limits regarding where and what you can buy. The conventional loan also does not have any income limits. Before you decide which type of loan is best for you, speak with a local, reputable lender who will analyze your finances and credit score. This is part of getting pre-qualified for a mortgage loan.

VA vs USDA Loan

The VA loan is another type of loan that requires no downpayment. However, it is only available to eligible military service members. The VA loan does not have an annual fee like the USDA loan, but….the VA loan does have a one-time “VA Funding Fee” which is either paid at closing or included in the loan. There are no requirements regarding the location of a house, but like the USDA loan, a house itself must not have any health or safety issues. Many eligible military service members use the VA loan when buying a house. A reputable lender will be able to help you decide which type of loan is best for you.

USDA vs FHA Loan

Many buyers, especially first-time buyers, decide between a USDA loan and FHA loan. Often times, the credit score required for the FHA loan is lower than what’s required for the USDA, VA and conventional loans. A downpayment of at least 3.5% is required when using a FHA loan, whereas the USDA loan has no downpayment requirement. There is also no location requirement for the FHA loan, although some condo and townhouse communities are not approved for the FHA loan. Just like the USDA loan, there is an upfront fee, as well as an annual fee known as mortgage insurance premium. A local, reputable lender will be able to help you decide which type of loan is best for you.

USDA Pros and Cons

Benefits of USDA Loans

There are quite a few advantages to using the USDA real estate loan. The USDA advantage includes:

- No down payment is required, the entire amount can be financed.

- USDA minimum loan amount…there is none!

- Gift money can be used to cover closing costs.

- Buyers can accept up to 6% of the purchase price from the seller to be used as closing cost concessions (Caution: In a seller’s market, its very difficult to obtain these concessions from a seller).

- There is no pre-payment penalty if you pay off your loan early.

- Interest rates are fixed and will not change.

- The loan can be used to purchase existing or newly constructed homes, or a home in a planned unit development. Some condos and manufactured homes are also eligible.

- The loan can be used to refinance an existing home.

- The upfront guarantee fee can be rolled into the loan amount above the appraised value.

Downside of USDA Loan / USDA Loan Cons

- You won’t be eligible for this loan is you earn more than the maximum allowable income ( a reputable local lender will be advise you of the current limits).

- You’re limited to buying in a pre-determined area. The USDA defines rural areas as “open countryside, rural towns” (places with fewer than 2.500 people).

- Eligibility requirements for the property itself apply. For example, the property must be considered “modest,” without luxury features, such as a pool.

- You must live in the home. No part of it can be used as a rental.

- There is an upfront guarantee fee (fortunately, it can be added to the loan, but will end up increasing the amount of your mortgage each month).

- These loans require a 2-step approval process. The lender issues final approval first, then it goes to the USDA for secondary approval. So, it takes longer to close on a house. Typically it takes about 45 days, whereas other types of loans can take about 30 days.

How to Find USDA Homes

The best way to find USDA homes is to contact a local real estate expert who knows the USDA areas. This will take the guesswork out of it for you, and make your home search easier. A local real estate expert will also know which houses are in good condition for this type of loan. Contact Melissa Spittel at the bottom of this page to learn more about buying a house with the USDA loan.

Search for Homes in Your Favorite Areas

Search for Homes in Carroll County MD

Are USDA Loans Bad?

USDA loans are great for buyers who don’t have money for a downpayment, and offer a variety of benefits to home buyers. These loans aren’t ideal to use in a seller’s market, though, because it can be difficult to compete with other buyers who are using a conventional loan or who have the ability to buy a house for cash. When buying a house in Maryland, you’ll need to check the USDA Maryland map to see if a house is located in a USDA area. When planning to buy a house with a USDA loan, it’s important to understand the details about the loan. A Maryland real estate expert can guide you each step of the way.

Learn More about Buying a House in Maryland!

Learn More on Melissa’s YouTube Channel

About the Author:

Melissa Spittel is a local real estate expert who serves Carroll County and the surrounding counties in Maryland. Her knowledge, skills and experience are invaluable when it comes to buying or selling a house. Her experience working with out-of-state buyers and sellers makes her a great relocation REALTOR®, and she is part of Coldwell Banker’s Relocation Team. Do you need a real estate expert in another part of Maryland? Or even in another state? Melissa can easily connect you with a REALTOR® from her wide network of real estate pros.